Alamy • Singles today know: If you're looking to meet that special someone, it's worth checking out Match.com, JDate, OKCupid, or one of the myriad other dating websites out there. But if you're looking to meet that special investment, you might want to visit Hedgez: Basically, it's a dating site that links up investors and hedge funds, based on the compatibility of their profiles. • Given the difficulty that millions of Americans have already faced with using the HealthCare.gov website, some may be worried: What if I don't manage to sign up for health care in time and have to pay the IRS a penalty? Well, as our friends at USA Today reminded us all today, there's not much to be afraid of. Thanks to how Congress wrote the Obamacare legislation, the IRS will have little leverage to force people to pay those fines ... er, taxes.

Alamy • Singles today know: If you're looking to meet that special someone, it's worth checking out Match.com, JDate, OKCupid, or one of the myriad other dating websites out there. But if you're looking to meet that special investment, you might want to visit Hedgez: Basically, it's a dating site that links up investors and hedge funds, based on the compatibility of their profiles. • Given the difficulty that millions of Americans have already faced with using the HealthCare.gov website, some may be worried: What if I don't manage to sign up for health care in time and have to pay the IRS a penalty? Well, as our friends at USA Today reminded us all today, there's not much to be afraid of. Thanks to how Congress wrote the Obamacare legislation, the IRS will have little leverage to force people to pay those fines ... er, taxes.

Wednesday, October 30, 2013

A 'Dating Site' for Hedge Funds, & 4 More Things to Know Today

Tuesday, October 29, 2013

Is Foreclosure Ever a Good Idea?

Over the last few years, since the crash of the housing bubble and in this troubled economy, many homeowners have homes worth significantly less than what they paid, greatly diminished incomes, and other issues. Foreclosing on a home has major ramifications that can last for years, but for some, foreclosure may seem like the only option. Here, we take a look at some of the details and alternatives.

Many Americans bought homes during the housing bubble which are now worth much, much less than the asking price at the time. There are many reasons home prices have fallen, resulting in underwater mortgages. As an example, entire neighborhoods were built in a booming frenzy by construction companies during the bubble. In some of these areas, the construction created a glut of housing, and many houses stayed vacant. The homeowners who bought into these ghost towns are faced with empty neighborhoods and homes valued at far less than what they owe. Other more established neighborhoods emptied out as homeowners defaulted on sub-prime mortgages, causing homes in the entire neighborhood to fall in value. The homes are hard to sell, even at a loss, and can be just as hard to rent out to others.

And it's no secret that incomes around the country have dropped. Most everyone knows someone who has lost a job and taken a pay cut upon returning to work. Mortgage payments which were easy to meet under better wages have now become increasingly harder to pay, and many homeowners are finding themselves struggling to stay on top of the bills.

So, while some bought homes they couldn't quite afford, lured by low interest rates and all-too-willing, unscrupulous lenders and they ended up in default. However, for many Americans, home purchases that seemed like a wise investment at the time have turned into financial disasters. Many are wondering what to do next with a mortgage that is too high, homes that won't sell for enough to pay for the mortgage, or homes which are simply unli! kely to sell at all.

Foreclosure is one way out of the game, but with steep implications. It can completely destroy one's credit rating for years to come, and make it difficult to get a needed loan later on. It could hurt a family's chance of renting if a credit report is part of the applicant screening process, thereby limiting rental options. Any open lines of credit may be lowered once the default goes on record, and some credit card companies may change other terms. Further, there can be steep tax implications come April 15.

If a homeowner is already behind on payments, these ramifications may already apply.

The advantages of foreclosure include being able to stay without paying rent for a while. In some states, this could be a year or longer, which could buy time to catch up financially, find better employment, or otherwise develop ways to increase income. During that time, it might also be possible to negotiate new terms with the bank, especially if the home is in a difficult housing market. However, we've all heard the horror stories about cut-throat practices by some lenders who have foreclosed on homes illegally, so it is still very risky.

An alternative to foreclosure is a short sale, although the negative impact to credit scores can be just as bad as a foreclosure on record. A short sale is an agreement with the bank to sell the house for less than what is owed, and the homeowner can be allowed to walk away with minimal cost, or given terms to pay back the deficiency which the homeowner can more easily handle financially.

Often, people facing these difficult choices are advised to seek other alternatives. If it's possible to secure more affordable living quarters (perhaps with a family member, for example), renting out the house can be an option bring in income and avoid foreclosure. However, this route can bring its own problems as well, especially if the tenants prove to be troublesome. The home will still require maintenance and homeowners fees.

While advice to rent the home out can be thrown around liberally and by people who mean well, it's not always an option. Some homeowners associations may have restrictions on renting, or it may even be banned, so it may not even be possible to rent the home. Even without a homeowner's association, many municipalities have laws which restrict rental terms. For example, in many college towns, year-round residents have worked to pass laws that keep homes from becoming college flop houses by encouraging local government to pass laws allowing no! more than two unrelated adults to live in one single-family home, or similar laws. Research on local laws will be required to determine if renting is actually an option.

Of course, none of these tips can replace legal advice from a qualified lawyer. Laws vary greatly by state and region, and the unique set of circumstances any homeowner is in vary as well, so there are no simple solutions when the mortgage has turned into a monster. Foreclosure can be a way out from under an enormous burden, but not without long-term consequences. It's important that anyone considering foreclosure consider all the options open to them and seek the advice of qualified professionals.

Sunday, October 27, 2013

Why Do Airlines Hedge Fuel Costs?

Most airlines in the U.S. today hedge fuel costs in a systematic fashion. Each quarter, they open new hedge positions in future quarters, with earlier periods tending to be more heavily hedged than periods further in the future.

If you asked airline executives why they hedge fuel, they would almost all say that since they sell most of their tickets several months in advance, they need to lock in some of their fuel costs in advance, too. However, most airlines hedge fuel one to two years out. Thus, they are hedging far beyond what is necessary to cover previously sold tickets. Most executives would probably claim that they do this in order to mitigate their risk, since it's difficult to pass fuel prices through to customers immediately.

This fuel-hedging strategy has questionable utility over the long term. Airlines that follow this practice are locking in some of their future fuel consumption each month, and so over time these companies' fuel costs are tied to the market price just as they would be if they did not hedge at all. The only difference is one of timing; hedging programs tend to smooth out the cost of fuel over time.

However, systematic hedging programs have very clear costs. Oil prices tend to be quite volatile, leading to high hedging premiums. Moreover, the relationship between oil prices and jet fuel is not constant, creating a risk that fuel hedges will be "ineffective". As a result, from a long-term investor's perspective, hedging fuel costs does not make very much sense. Over a typical economic cycle, hedging losses will tend to outweigh hedging gains.

Swimming against the tide

Alone among legacy carriers, US Airways (NYSE: LCC ) abandoned its fuel-hedging program after the Great Recession. The company determined that the cost of hedging premiums was excessive.

Moreover, by locking in fuel prices through collars, swaps, forward price contracts, or similar hedging instruments, airlines lock in a minimum fuel price as well as a maximum price. In the event of a sudden economic shock -- something like the Great Recession -- the airline would face low demand, but fuel prices would be locked in at an above-market price by the hedges. In other words, hedges provide the least protection in the most dangerous economic environment.

The move away from fuel hedging has worked out well for US Airways -- despite the fact that oil prices have risen dramatically from 2009 to today. Since 2010, US Airways has paid a lower average fuel price compared to each of the four largest airlines in the country -- AMR (NASDAQOTH: AAMRQ ) , Delta Air Lines (NYSE: DAL ) , Southwest Airlines (NYSE: LUV ) , and United Continental (NYSE: UAL ) -- all of which use fuel hedges extensively.

Airline yearly average fuel prices (2010-present):

Source: Airline annual 10-K reports

In 2011, when fuel prices skyrocketed due to strong demand and fears about the Arab Spring, US Airways paid slightly more for fuel than most of its competitors. However, this has been balanced out by lower fuel bills in every other year, when competitors' hedge premiums went to waste.

10 Best Insurance Stocks To Buy For 2014

Over the full period, US Airways has saved anywhere from $0.01 per gallon (compared to AMR), to $0.09 per gallon (compared to Southwest). In a declining fuel price environment, US Airways would have shown an even bigger advantage. Since the major airlines use billions of gallons of jet fuel each year, they are potentially losing tens or even hundreds of millions of dollars annually from hedging.

Back to square one

Over the past several years, US Airways has shown quite convincingly that the costs of fuel hedging outweigh the benefits. Even in a rising fuel price environment -- when hedging should offer the most benefits -- US Airways has still paid less than competitors for fuel, on average. So why do most of US Airways' competitors continue to hedge?

The real reason is most likely that executives want to increase the predictability of earnings. By hedging, airlines restrain their profit growth when fuel prices drop while mitigating the drag of fuel price increases. Airline executives look better to shareholders in the short-run if they can make earnings relatively predictable.

However, hedging costs are significant over time. For long-term investors, having a higher long-term earnings stream should be more important than artificially keeping earnings steady from year to year, as long as a company can maintain comfortable liquidity throughout the business cycle. (Major airlines tend to hold billions of dollars in cash, so this shouldn't be a major issue.) Unfortunately, only US Airways is really looking out for long-term investors' interests when it comes to fuel hedging.

Do you want to hedge your own exposure to oil price shocks? If so, you should check out The Motley Fool's special report on the energy sector: "3 Stocks for $100 Oil". This report points out some intriguing energy plays that could help your portfolio if oil prices continue to rise. For FREE access, simply click here now.

Saturday, October 26, 2013

Top 10 Blue Chip Companies To Watch In Right Now

It is no longer news that International Business Machine (IBM) released disappointing 2013 third quarter results. It is also no longer news that the stock has taken a beating since then from $186.73 per share it traded at the close of business just before the third quarter financials were released to the investing public on Wednesday, Oct. 16. The negative reactions of investors to the third quarter results were noticed during the extended hours of trading on that same day when the stock took a dip from $186.73 to $175.99 per share. That sudden dip in IBM�� stock price amounts to a loss of about 6% per share within a space of a few hours after the release of the third quarter results.

Really, IBM needs no introduction to a large number of the investing public because it is renowned as one of the blue chip companies with the best stock rating many love to own. In the last decade, IBM maintained a good rating as the only tech company that offered consistent yearly dividend increases. IBM is a tech company that has survived three eras of computing technology transitions. In the last two decades, the company has transitioned from the mainframe era to the PC era and now to the era of mobile computing technology where it is taking a foothold in the software and services line of business and declining its operations from being a pure hardware producing company.

Top 10 Blue Chip Companies To Watch In Right Now: Apple Inc.(AAPL)

Apple Inc., together with subsidiaries, designs, manufactures, and markets personal computers, mobile communication and media devices, and portable digital music players, as well as sells related software, services, peripherals, networking solutions, and third-party digital content and applications worldwide. The company sells its products worldwide through its online stores, retail stores, direct sales force, third-party wholesalers, resellers, and value-added resellers. In addition, it sells third-party Mac, iPhone, iPad, and iPod compatible products, including application software, printers, storage devices, speakers, headphones, and other accessories and peripherals through its online and retail stores; and digital content and applications through the iTunes Store. The company sells its products to consumer, small and mid-sized business, education, enterprise, government, and creative markets. As of September 25, 2010, it had 317 retail stores, including 233 stores in the United States and 84 stores internationally. The company, formerly known as Apple Computer, Inc., was founded in 1976 and is headquartered in Cupertino, California.

Advisors' Opinion:- [By Rich Smith]

Over in Russia, market-leading cell phone provider Mobile TeleSystems (NYSE: MBT ) has just confirmed that, as of 2012, it no longer sells Apple's (NASDAQ: AAPL ) new iPhone models to its customers directly. The company does still stock, and sell, some older iPhone models. But for iPhone5 and on up, MTS now answers phone calls from Apple with a Spasibo, ne nada. ("Thanks, but no thanks.")

Top 10 Blue Chip Companies To Watch In Right Now: Colgate-Palmolive Company(CL)

Colgate-Palmolive Company, together with its subsidiaries, manufactures and markets consumer products worldwide. It offers oral care products, including toothpaste, toothbrushes, and mouth rinses, as well as dental floss and pharmaceutical products for dentists and other oral health professionals; personal care products, such as liquid hand soap, shower gels, bar soaps, deodorants, antiperspirants, shampoos, and conditioners; and home care products comprising laundry and dishwashing detergents, fabric conditioners, household cleaners, bleaches, dishwashing liquids, and oil soaps. The company offers its oral, personal, and home care products under the Colgate Total, Colgate Max Fresh, Colgate 360 Advisors' Opinion:

- [By Eric Volkman]

It's one of the steadiest dividend payers on the market, and it's continuing to fly level. Colgate-Palmolive (NYSE: CL ) has declared a fresh quarterly common stock dividend, which is to be $0.34 per share, paid on August 15 to shareholders of record as of July 23. That amount matches the firm's previous distribution; this was paid in May. Prior to that, Colgate-Palmolive handed out $0.31 per share.

- [By Dan Caplinger]

Lately, Johnson & Johnson has presented two different faces to investors. On one hand, the company has faced the challenge of dealing with a weak consumer-products business, as multiple recalls and close regulatory oversight of its production facilities have exacerbated J&J's problems. With its more focused consumer-goods business, Colgate-Palmolive (NYSE: CL ) has worked harder at taking advantage of international growth opportunities than many of its rivals, and Colgate's strong overseas sales, in comparison to J&J's international weakness, show the effectiveness of that strategy. In particular, Asia has been a focus point for Colgate, with revenue from the region having risen 9% year over year compared with less than 3% growth overall. Moreover, Latin America represents Colgate's biggest region for sales, with more than half again the revenue its U.S. segment produces.

- [By Jon C. Ogg]

Colgate-Palmolive Co. (NYSE: CL) was raised to Overweight from Equal Weight and the price target is now $68 (versus a $59.93 close) at Morgan Stanley.

Top 5 China Stocks To Own Right Now: International Business Machines Corporation(IBM)

International Business Machines Corporation (IBM) provides information technology (IT) products and services worldwide. Its Global Technology Services segment provides IT infrastructure and business process services, including strategic outsourcing, process, integrated technology, and maintenance services, as well as technology-based support services. The company?s Global Business Services segment offers consulting and systems integration, and application management services. Its Software segment offers middleware and operating systems software, such as WebSphere software to integrate and manage business processes; information management software for database and enterprise content management, information integration, data warehousing, business analytics and intelligence, performance management, and predictive analytics; Tivoli software for identity management, data security, storage management, and datacenter automation; Lotus software for collaboration, messaging, and so cial networking; rational software to support software development for IT and embedded systems; business intelligence software, which provides querying and forecasting tools; SPSS predictive analytics software to predict outcomes and act on that insight; and operating systems software. Its Systems and Technology segment provides computing and storage solutions, including servers, disk and tape storage systems and software, point-of-sale retail systems, and microelectronics. The company?s Global Financing segment provides lease and loan financing to end users and internal clients; commercial financing to dealers and remarketers of IT products; and remanufacturing and remarketing services. It serves financial services, public, industrial, distribution, communications, and general business sectors. The company was formerly known as Computing-Tabulating-Recording Co. and changed its name to International Business Machines Corporation in 1924. IBM was founded in 1910 and is based in Armonk, New York.

Advisors' Opinion:- [By Caroline Bennett]

For the fourth year in a row, IBM (NYSE: IBM ) has placed first in International Data Corp.'s worldwide rankings for market share for enterprise social software, IBM announced yesterday.

Top 10 Blue Chip Companies To Watch In Right Now: Chevron Corporation(CVX)

Chevron Corporation, through its subsidiaries, engages in petroleum, chemicals, mining, power generation, and energy operations worldwide. It operates in two segments, Upstream and Downstream. The Upstream segment involves in the exploration, development, and production of crude oil and natural gas; processing, liquefaction, transportation, and regasification associated with liquefied natural gas; transportation of crude oil through pipelines; and transportation, storage, and marketing of natural gas, as well as holds interest in a gas-to-liquids project. The Downstream segment engages in the refining of crude oil into petroleum products; marketing of crude oil and refined products primarily under the Chevron, Texaco, and Caltex brand names; transportation of crude oil and refined products by pipeline, marine vessel, motor equipment, and rail car; and manufacture and marketing of commodity petrochemicals, plastics for industrial uses, and fuel and lubricant additives. It a lso produces and markets coal and molybdenum; and holds interests in 13 power assets with a total operating capacity of approximately 3,100 megawatts, as well as involves in cash management and debt financing activities, insurance operations, real estate activities, energy services, and alternative fuels and technology business. Chevron Corporation has a joint venture agreement with China National Petroleum Corporation. The company was formerly known as ChevronTexaco Corp. and changed its name to Chevron Corporation in May 2005. Chevron Corporation was founded in 1879 and is based in San Ramon, California.

Advisors' Opinion:- [By Brian Stoffel]

2. Chevron (NYSE: CVX ) , P/E of 9.5

Sometimes, it can be tough for large oil companies to get much love from Wall Street. With a market cap of more than $240 billion and sales expected to remain relatively flat over the next four years, it's understandable that most investors aren't willing to pay a premium for Chevron. - [By Anders Bylund]

Exxon is a bit of an anomaly, as the company manages to stick close to the Dow average here, dishing out 45.7% of its free cash, while the broader oil industry tends to jump around at the whim of changing petroleum prices. Fellow oil-producer Chevron (NYSE: CVX ) isn't so lucky, spending 86% of its free cash on dividend checks. The roles were the same a year earlier, though the magnitudes were different: Chevron invested 41.8% of its 2011 cash flow in dividends, while Exxon's ratio was an even lower 37%.

- [By Laura Brodbeck]

Friday

Earnings Expected From: Chevron Corporation (NYSE: CVX), OM Group, Inc. (NYSE: OMG), Public Storage (NYSE: PSA) Economic Releases Expected: �US ISM manufacturing index, Canadian manufacturing PMI, British manufacturing PMI, Norwegian unemployment ratePosted-In: Bank Of England Federal ReserveNews Eurozone Commodities Previews Global Economics Federal Reserve After-Hours Center Markets Trading Ideas Best of Benzinga

- [By M. Joy Hayes, Joy]

Thus, a failure to protect these employees arguably puts Exxon at a competitive disadvantage against companies like Chevron (NYSE: CVX ) , Shell Oil (NYSE: RDS-A ) , and BP (NYSE: BP ) which, according to the Human Rights Campaign, all offer better protections and benefits for LGBT employees.

Top 10 Blue Chip Companies To Watch In Right Now: Philip Morris International Inc(PM)

Philip Morris International Inc., through its subsidiaries, engages in the manufacture and sale of cigarettes and other tobacco products in markets outside of the United States. Its international product brand line comprises Marlboro, Merit, Parliament, Virginia Slims, L&M, Chesterfield, Bond Street, Lark, Muratti, Next, Philip Morris, and Red & White. The company also offers its products under the A Mild, Dji Sam Soe, and A Hijau in Indonesia; Diana in Italy; Optima and Apollo-Soyuz in the Russian Federation; Morven Gold in Pakistan; Boston in Colombia; Belmont, Canadian Classics, and Number 7 in Canada; Best and Classic in Serbia; f6 in Germany; Delicados in Mexico; Assos in Greece; and Petra in the Czech Republic and Slovakia. It operates primarily in the European Union, Eastern Europe, the Middle East, Africa, Asia, Canada, and Latin America. The company is based in New York, New York.

Advisors' Opinion:- [By Holly LaFon]

Company % of Assets Pepsico (PEP) 3.4 Philip Morris (PM) 2.3 Tesco PLC ADR (TSCO) 2.1 Molson Coors Brewing (TAP) 2.1 Microsoft (MSFT) 1.9 Merck (MRK) 1.9 Procter & Gamble (PG) 1.8 Avon Products (AVN) 1.6 Wal��art (WMT) 1.6 Medtronic 1.6 Hospira (HSP) 1.5 BP (BP) 1.4 Medco Health Solutions (MHS) 1.3 Johnson & Johnson (JNJ) 1.3 Unilever NV (UL) 1.3

Jeff is also optimistic about natural gas and believes the recession in Europe could be setting up "a generational buying opportunity." - [By Rich Duprey]

Global tobacco giant�Philip Morris International (NYSE: PM ) announced this morning its second-quarter dividend of $0.85 per share, the same rate it's paid for the past three quarters after raising the payout 10% from $0.77 per share.

- [By Tim McAleenan Jr.]

And lastly, Mankiw mentions emerging markets. If you want to bet against the United States dollar and own a company that generates all of its profits outside the United States, it could be useful to take a look at Philip Morris International (PM). Asia makes up 37% of its profits. The Middle East, Africa, and Eastern Europe make up 27% of its profits. Smoking rates in countries like Indonesia are increasing at 10-25% annual rates. The Marlboro brand is gaining market share in Asia. The company is planning aggressive expansion into Central Africa. If you want emerging markets exposure, Philip Morris International could be a decent way to cover your bases.

Top 10 Blue Chip Companies To Watch In Right Now: Visa Inc.(V)

Visa Inc., a payments technology company, engages in the operation of retail electronic payments network worldwide. It facilitates commerce through the transfer of value and information among financial institutions, merchants, consumers, businesses, and government entities. The company owns and operates VisaNet, a global processing platform that provides transaction processing services. It also offers a range of payments platforms, which enable credit, charge, deferred debit, debit, and prepaid payments, as well as cash access for consumers, businesses, and government entities. The company provides its payment platforms under the Visa, Visa Electron, PLUS, and Interlink brand names. In addition, it offers value-added services, including risk management, issuer processing, loyalty, dispute management, value-added information, and CyberSource-branded services. The company is headquartered in San Francisco, California.

Advisors' Opinion:- [By Lennox Yieke]

In light of this, payments bigwigs Visa (NYSE: V ) and MasterCard (NYSE: MA ) have increased their presence in the continent. Not only have Visa and MasterCard increased issuance of plastic money, but they have also made bold mobile money initiatives. Could this spur the next round of prolonged growth for the two bigwigs?

- [By Victor Reklaitis]

The Dow Jones Industrial Average (DJIA) rose 71 points, or 0.5%, to 15,067. Visa Inc. (V) �showed the largest gain among blue chips with its 1% advance, while Verizon Communications Inc. (VZ) � and Merck & Co. (MRK) �were the biggest losers as they each fell 0.6%.

- [By Charles Carlson]

The only three Dow stocks that do not are actually, interestingly, two of the newest members, Goldman Sachs (GS) and Visa (V), and the third stock is UnitedHealth Group (UNH), which is also a fairly new member to the Dow.

- [By Rich Smith]

Good news

The good news, though, is that in many cases at least you can get the same peace of mind from an extended warranty (even if you never get to use it) by simply buying with a credit card. Most products you buy, after all, come with a manufacturer's warranty built right in. And depending on the card you use to buy an item, MasterCard (NYSE: MA ) or Visa (NYSE: V ) for example will often automatically double the length of any manufacturer's warranty, adding as much as a year to your warranty period free of charge.

Top 10 Blue Chip Companies To Watch In Right Now: McDonald's Corporation(MCD)

McDonald?s Corporation, together with its subsidiaries, operates as a worldwide foodservice retailer. It franchises and operates McDonald?s restaurants that offer various food items, soft drinks, coffee, and other beverages. As of December 31, 2009, the company operated 32,478 restaurants in 117 countries, of which 26,216 were operated by franchisees; and 6,262 were operated by the company. McDonald?s Corporation was founded in 1948 and is based in Oak Brook, Illinois.

Advisors' Opinion:- [By Jim Jubak]

McDonald's (MCD) customers are getting squeezed and so, therefore, is McDonald's.

For the third quarter, comparable store sales grew by just 0.7% in the United States. That's down from 1% comparable store sales growth in the second quarter. Global comparable sales climbed by 0.9%. Wall Street had been expecting 1% growth.

Friday, October 25, 2013

Bill Gross tells Icahn to leave Apple alone

NEW YORK (CNNMoney) Shareholder activist Carl Icahn is turning up the heat on Apple (AAPL, Fortune 500). And that seems to be making bond king Bill Gross uncomfortable.

NEW YORK (CNNMoney) Shareholder activist Carl Icahn is turning up the heat on Apple (AAPL, Fortune 500). And that seems to be making bond king Bill Gross uncomfortable. Gross, who runs the giant bond fund Pimco Total Return (PTTAX), raised eyebrows Thursday after he picked a Twitter fight with Icahn, who had just demanded that Apple buy back $150 billion of its own stock.

"Icahn should leave #Apple alone & spend more time like Bill Gates," Gross said on Twitter, referring to the Microsoft (MSFT, Fortune 500) chairman who's now famous for his philanthropic efforts. "If #Icahn's so smart, use it to help people not yourself."

The harsh words were surprising coming from Gross, an avid yoga fan who prefers to wear his ties undone. There's also the fact that Gross is known more for his calls on Treasuries and interest rates, not tech stocks.

But it's worth remembering that Apple sold $17 billion worth of bonds in May, the largest corporate debt offering in history.

For the record, Pimco doesn't appear to own any Apple bonds, which are not listed among the holdings in the ETF that tracks Pimco's Investment Grade Corporate Bond (CORP) fund. It's also not listed as holding in the ETF that mirrors the Total Return Fund (BOND).

Pimco does own a small stake in Apple's common stock, according to FactSet. A spokesman did not immediately respond to questions about whether Pimco owned any Apple bonds.

In theory, Icahn's plan for a huge stock repurchase poses a threat to Apple's credit quality. If Apple gives in to Icahn's demands, it would end up with less cash and more debt on its balance sheet.

New iPhone a yawn? Apple is still a bargain

New iPhone a yawn? Apple is still a bargain This is troubling for Apple bondholders, since part of the company's appeal is that it has a lot of cash and not much debt. There aren't that many high-quality corporate bonds out there. Microsoft (MSFT, Fortune 500) and Johnson & Johnson (JNJ, Fortune 500) are among the few AAA-rated issuers. Apple's bonds are rated AA by the rating agencies.

Hot Heal Care Companies To Watch In Right Now

What's more, Apple has already shown a willingness to listen to activist investors, including David Einhorn of Greenlight Capital.

Although Apple did not agree to Einhorn's proposal to issue preferred shares, Apple did increase its existing buyback program to $60 billion from $10 billion in April. The bond sale, a surprising move by the usually fiscally conservative Apple, was done to help finance the repurchase of stock.

Gary Jenkins, credit analyst at Swordfish Research, pointed out that bondholders are nervous because Apple already made a move to appease a vocal shareholder. So that makes it more likely that Apple may do something to quiet Icahn,

While Apple may not borrow as much as Icahn wants, "they probably will gradually change the structure of the balance sheet over time so that the credit profile is more in line with a single A rated credit," said Jenkins.

Still, there are reasons to doubt that Icahn will be successful, despite his veiled threat of a proxy fight.

For one, Apple's share price has risen 30% since it upped its share buyback program in April. So buying back stock now would be more expensive and seems less necessary.

Additionally, Icahn lost a similar battle at Transocean (RIG) in May, when shareholders approved a smaller dividend increase than he wanted.

The real threat for Apple bond holders is the general trend of rising interest rates, said ! Jody Luri! e, corporate credit analyst at Janney Capital Markets.

She said Icahn is not an immediate concern, but acknowledged that "there is a certain level of discomfort when an activist investor comes into company and stirs up talk of additional shareholder rewards."

But in a somewhat surprising show of restraint, Icahn didn't push back against Gross. Speaking on CNBC Thursday, the notoriously scrappy New York native, who publicly sparred with hedge fund manager Bill Ackman this year, said he respects Gross and other top investors who have criticized his methods.

"I think that Bill Gross certainly has a right to his opinion," said Icahn, who proceeded to compare his push to get Apple to reward shareholders with President Theodore Roosevelt's trust busting campaign in the early 1900s. ![]()

Monday, October 21, 2013

At Long Last, Has Apple Hooked Up With Taiwan Semiconductor?

Investors have been talking about Apple (NASDAQ: AAPL ) hooking up with Taiwan Semiconductor (NYSE: TSM ) for years. However, switching chip foundries is much easier said than done and the transition can take quite a while. Well, DIGITIMES now reports that the long-rumored deal has finally been inked as Apple continues to distances itself from Samsung.

Taiwan Semiconductor has inked a three-year deal with the Mac maker, according to the Taiwanese publication's supply chain sources. The chip manufacturer will provide the next three generations of A-chips to Apple, which will progress to 20-nanometer, 16-nanometer, and then 10-nanometer manufacturing processes. Currently, Apple's latest A6 is built on Samsung's 32-nanometer node.

Test runs for the A8 may start as soon as next month, with 20-nanometer production ramping up next year to correspond with new infrastructure slated for the same time frame. Some of the production capacity could get upgraded later for 16-nanometer chips. Taiwan Semiconductor is supposedly scheduled to mass produce the A9 and A9X in the third quarter of next year.

DIGITIMES says the A8 will power the iPhone due out in 2014, and the A9 and A9X subsequently should be found in the 2015 models. Taiwan Semiconductor has already begun early stage risk production for its 20-nanometer node, which commenced in the first quarter.

There was no mention of whether or not this deal was exclusive or not. That still leaves the possibility of Apple tapping Intel (NASDAQ: INTC ) for foundry services, another partnership that's been rumored a time or two. Intel ex-CEO Paul Otellini admitted that not partnering with Apple on the original iPhone was one of his biggest regrets, and perhaps new CEO Brian Krzanich will make up for it. The chip giant has already begun to offer foundry services to smaller customers in order to utilize its idle capacity and unrivaled manufacturing prowess.

Apple surely wants to cut Samsung out of the loop, and Taiwan Semiconductor and Intel would be happy to pick up the slack.

It's incredible to think just how much of our digital and technological lives are almost entirely shaped and molded by just a handful of companies. Find out "Who Will Win the War Between the 5 Biggest Tech Stocks?" in The Motley Fool's latest free report, which details the knock-down, drag-out battle being waged by the five kings of tech. Click here to keep reading.

Sunday, October 20, 2013

QE Tapering? Plenty Of USD Bulls At ICU Assuming So

The price action that has hit the market in the past few weeks is nothing short of impressive, with commentators struggling to make sense out of all this mess in prices. The market is presently governed on such a multi-theme basis that makes it both a mine of opportunities yet at the same time such an irrational place.

If the market did not have enough tumultuous' headlines, which culminated yesterday with a -6.23% fall in the Nikkei, Fed watcher Jon Hilsenrath put out an article before the U.S. close suggesting that Bernanke is still miles away from considering any kind of tightening in rates as hopes have built up on a possible tapering in the next few months.

Kathy Lien, Co-Founder at BKAM, thinks Hilsenrath's article is not that supportive for stocks because, as Lien points out, "his conclusion of the Fed no way near raising interest rates is based on the U.S. economy not [being] strong enough to handle it."

Where are we at? From USD ruling to sustained weakness

In the second quarter of 2013, markets have gradually turned the thought of tapering into a reality, as exemplified by the broad-based USD gains through May, only to suffer a massive washout which sees still no end in sight. Is the market realizing that tapering will not happen that quick, thus the realization of an excessive pricing of a Fed QE exit strategy?

Adam Button, editor at Forexlive, makes an analogy of the market by suggesting us all to use our imagination to picture 100 people in a room, trading billions of dollars and with no idea of what's going on: "That's Wall Street at the moment," Button says.

Button has identified four main themes underway in the market at the moment. The first is the rout in the Nikkei, defined as "irrational exuberance," secondly, there is a massive unwinding of carry trades and bets on emerging markets.

Top 5 Penny Stocks To Own For 2014

Th! irdly, "this sparked a rush from emerging markets to yen, dollars, euro and sterling while AUD was smoked by carry trade unwinds. The idea that the Fed would taper kept the dollar buoyant at the same time," Button added.

The fourth item is actually the idea of tapering not coming into fruition in the near term, speculating that "with conditions like this and bond yields up 50 bps, the Fed simply will not taper," which suggest further room for USD.

Markets are clearly experiencing a dislocation of assets, but we are still in a very indecisive early stage where the motives behind current moves are being driven by dangerous assumptions without enough justification, it seems.

Moves likely to appease until FOMC

But until Ben Bernanke speaks at next week's FOMC press conference, new information to decipher the actual puzzle is close to 0. From his speech we will know whether the tumultuous market conditions are set to continue or abate. The former is the most likely though, as the ball of expectations/dislocations has now gotten too big to easily ignore.

According to Greg McKenna, Founder at GlobalFX, "the talk of tapering next week from the Fed is likely even if they are going to try to do it in a way that is least disruptive to markets."

Source: QE Tapering? Plenty Of USD Bulls At ICU Assuming SoDisclosure: I have no positions in any stocks mentioned, and no plans to initiate any positions within the next 72 hours. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it. I have no business relationship with any company whose stock is mentioned in this article. (More...)

Friday, October 18, 2013

J.C. Penney Latest Retailer to Open on Thanksgiving

Patrick T. Fallon/Bloomberg via Getty Images NEW YORK -- J.C. Penney is opening its doors on Thanksgiving evening to kick off the holiday shopping season, as the beleaguered retailer hopes to get back in the game for the crucial selling period. The Plano, Texas-based chain will be opening most of its 1,100 stores at 8 p.m., the same as rival Macy's (M). The Thanksgiving evening opening is much earlier than last year, when Penney didn't open until 6 a.m. Friday. That made the retailer one of the laggards for the unofficial kickoff to the season. J.C. Penney (JCP) is also bringing back a tradition it ditched last year: it will give away nearly 2 million holiday snow globes starting at 4 a.m. on the Friday after the turkey feast. "Obviously, we were one of the last to open [last year]," said Tony Bartlett, Penney's executive vice president of stores. But he noted this year, "We're all in." He promised that Penney's deals will be at least as good as two years ago and will be much better than last year, when Penney gave away buttons tied to a prize giveaway. Penney is also hiring at least 35,000 seasonal workers for the holidays, nearly 50 percent more than a year ago. The holiday plan is yet another example of how Penney is unraveling the strategies of its former CEO Ron Johnson, who was ousted in April after 17 months on the job amid a botched up plan to reinvent the retailer. Johnson was fired two months after the company announced horrific fourth-quarter results that covered the holiday shopping season. That ended a fiscal year, which finished Feb. 2, in which the Penney amassed almost a billion dollars in losses and a 25 percent drop in sales. Penney brought back Johnson's predecessor, Mike Ullman, as CEO. He is restoring frequent sales and basic merchandise that were eliminated by Johnson who was aiming to attract a more affluent, younger shopper. Shares were down 12 cents to close at $7.35 Thursday and have lost 63 percent of their value since the beginning of the year. The stock has lost 83 percent of its value since early February of last year. Stores are ushering the holiday season earlier every year, creeping into Thanksgiving. Macy's scheduled 8 p.m. opening on Thanksgiving compares with its midnight Friday opening in 2012. Last year, Target (TGT) opened its doors at 9 p.m. on Thanksgiving, three hours earlier than the previous year. Walmart Stores (WMT), the world's largest retailer, began the early bird specials at 8 p.m on the holiday, two hours earlier than in 2011. A growing number of mall-based clothing stores such as Gap (GPS) also have opened their doors on Thanksgiving Day. Target, Walmart and Gap haven't yet announced their plans for the Thanksgiving weekend.

Patrick T. Fallon/Bloomberg via Getty Images NEW YORK -- J.C. Penney is opening its doors on Thanksgiving evening to kick off the holiday shopping season, as the beleaguered retailer hopes to get back in the game for the crucial selling period. The Plano, Texas-based chain will be opening most of its 1,100 stores at 8 p.m., the same as rival Macy's (M). The Thanksgiving evening opening is much earlier than last year, when Penney didn't open until 6 a.m. Friday. That made the retailer one of the laggards for the unofficial kickoff to the season. J.C. Penney (JCP) is also bringing back a tradition it ditched last year: it will give away nearly 2 million holiday snow globes starting at 4 a.m. on the Friday after the turkey feast. "Obviously, we were one of the last to open [last year]," said Tony Bartlett, Penney's executive vice president of stores. But he noted this year, "We're all in." He promised that Penney's deals will be at least as good as two years ago and will be much better than last year, when Penney gave away buttons tied to a prize giveaway. Penney is also hiring at least 35,000 seasonal workers for the holidays, nearly 50 percent more than a year ago. The holiday plan is yet another example of how Penney is unraveling the strategies of its former CEO Ron Johnson, who was ousted in April after 17 months on the job amid a botched up plan to reinvent the retailer. Johnson was fired two months after the company announced horrific fourth-quarter results that covered the holiday shopping season. That ended a fiscal year, which finished Feb. 2, in which the Penney amassed almost a billion dollars in losses and a 25 percent drop in sales. Penney brought back Johnson's predecessor, Mike Ullman, as CEO. He is restoring frequent sales and basic merchandise that were eliminated by Johnson who was aiming to attract a more affluent, younger shopper. Shares were down 12 cents to close at $7.35 Thursday and have lost 63 percent of their value since the beginning of the year. The stock has lost 83 percent of its value since early February of last year. Stores are ushering the holiday season earlier every year, creeping into Thanksgiving. Macy's scheduled 8 p.m. opening on Thanksgiving compares with its midnight Friday opening in 2012. Last year, Target (TGT) opened its doors at 9 p.m. on Thanksgiving, three hours earlier than the previous year. Walmart Stores (WMT), the world's largest retailer, began the early bird specials at 8 p.m on the holiday, two hours earlier than in 2011. A growing number of mall-based clothing stores such as Gap (GPS) also have opened their doors on Thanksgiving Day. Target, Walmart and Gap haven't yet announced their plans for the Thanksgiving weekend.

A. Guns B. Knives C. Pepper spray bomb

Thursday, October 17, 2013

Jim Cramer's 6 Stocks in 60 Seconds: CLB PPG NUE ALKS DDD CLX (Update 1)

10 Best Gold Stocks To Invest In 2014

Check out Jim Cramer's latest trading recommendations on "Action Alerts Plus". (Updates from 10:46 a.m. ET with closing information.)

NEW YORK (TheStreet) -- Here's what Jim Cramer had to say on CNBC's "Squawk on the Street" Thursday.

Core Laboratories (CLB) may have found the country's largest oil field, Cramer said. If so, Pioneer Natural Resources (PXD) will be the main beneficiary. CLB jumped 8.5% to $189.85.

PPG Industries (PPG) "has fabulous margins" and CEO Charles Bunch continues to deliver, Cramer said. PPG was up 5% to $174.47. Cramer was "thrilled" Nucor (NUE) was finally able to beat earnings estimates after missing for so many quarters. NUE rose 2% to $50.79. Alkermes (ALKS) has a few anti-opiate drugs and Cramer believes in the company and CEO Richard Pops. ALKS vaulted 8.5% to $35.38. Cramer said he was looking for technology companies and found that many investors were piling into 3D Systems (DDD) and other 3-D printing stocks. DDD was 2.7% higher at $56.76. Morgan Stanley downgraded Clorox (CLX) to sell, based on valuation. Cramer agreed, but also argued that the company has a 3.3% dividend yield and great management. CLX fell nearly 1% to $85.25. To sign up for Jim Cramer's free Booyah! newsletter, with all of his latest articles and videos, please click here. -- Written by Bret Kenwell in Petoskey, Mich. Follow @BretKenwell

Wednesday, October 16, 2013

Advance Auto Parts buying General Parts for $2B

As part of the transaction targeted to close by late 2013 or early 2014, Advance Auto will get 1,246 company operated stores and 1,418 independently owned Carquest locations. Its shares soared in premarket trading.

The Roanoke, Va., seller of auto parts and batteries currently operates more than 4,015 stores in the U.S., Puerto Rico and the Virgin Islands. General Parts is a privately held distributor and supplier of original equipment and aftermarket replacement products for commercial markets operating under the Carquest and Worldpac brands. The combined company will be based in Roanoke, Va., and continue to have a presence in Raleigh, N.C.

WEDNESDAY STOCKS: How markets are doing

Advance Auto CEO Darren Jackson said the transaction provides a "compelling strategic opportunity" to expand the company's geographic presence. In January, the company acquired privately held Northeast car parts supplier B.W.P. Distributors Inc., accelerating its growth in the Northeast.

Advance Auto also said Wednesday it expects third-quarter earnings of $1.42 per share on revenue of $1.52 billion, compared with year-ago earnings of $1.21 per share on revenue of $1.46 billion. Revenue at stores open at least a year is expected to decrease 2 percent. That's an important measure for retailers because it excludes results from newly opened or closed stores.

Analysts polled by FactSet predict earnings of $1.31 per share on revenue of $1.55 billion.

The company on Wednesday also reaffirmed its full-year adjusted earnings forecast of between $5.30 and $5.45. Analysts expect $5.55 per share.

When vehicle sales tumbled a few years ago, auto parts retailers such as Advance Auto Parts got a sales boost, as more Americans kept their vehicles longer and invested mo! re in keeping them running.

But Americans have been buying new cars and trucks at a healthy pace in recent months, fueled by low interest rates, better credit availability and aging cars that need replacement.

Tuesday, October 15, 2013

Hot Dividend Companies To Watch For 2014

For dividend investors, there’s good news … and bad news.

The good news is that, if you’re looking for income, it sure hasn’t been hard to find.�As of the second quarter’s end, the percentage of stocks paying dividends in the�S&P 500�was sitting at a 15-year high. And zooming in on just the last decade, aggregate dividend payments have doubled overall.

The bad news, though, is that many dividend-paying stocks sport misleading headline yields or unsustainable payouts — hardly the kind of income stock you want to snatch up for the long haul, or as a way to weather the current political menu of a government shutdown for dinner and the debt ceiling crisis for dessert.

With that in mind, we sorted through piles of dividend stocks to find some that�do�offer sustainable, surefire payouts for loyal shareholders thanks to impressive payout histories and sustainable payout ratios.

Hot Dividend Companies To Watch For 2014: Freeport-McMoran Copper & Gold Inc.(FCX)

Freeport-McMoRan Copper & Gold Inc. engages in the exploration, mining, and production of mineral resources. The company primarily explores for copper, gold, molybdenum, silver, and cobalt. It holds interests in various properties, located in North and South America; the Grasberg minerals district in Indonesia; and the Tenke Fungurume minerals district in the Democratic Republic of Congo. As of December 31, 2010, the company?s consolidated recoverable proven and probable reserves totaled 120.5 billion pounds of copper, 35.5 million ounces of gold, 3.39 billion pounds of molybdenum, 325.0 million ounces of silver, and 0.75 billion pounds of cobalt. The company was founded in 1987 and is headquartered in Phoenix, Arizona.

Advisors' Opinion:- [By John Divine]

Freeport-McMoRan Copper & Gold (NYSE: FCX ) rounds out the list of today's laggards, with a 2.3% loss. This is the third straight day of declines for the copper miner, which continues to struggle with market repercussions from a deadly mining disaster at one of its locations in Indonesia. The lost production from the closed mine is estimated to be around $15 million per day.

- [By Selena Maranjian]

Finally, Appaloosa Management's biggest closed positions included Oracle�and the PowerShares QQQ ETF. Other closed positions of interest include Freeport-McMoRan Copper & Gold (NYSE: FCX ) . The world's largest publicly traded copper producer, recently yielding 3.8%, has seen its stock slump in response to a tragic and deadly mine disaster in Indonesia. It had already been hurt by the price of copper falling and growth in China slowing as well as by labor strikes. The company has diversified its operations considerably by buying a pair of oil and gas producers.

Hot Dividend Companies To Watch For 2014: TotalFinaElf S.A.(TOT)

TOTAL S.A., together with its subsidiaries, operates as an integrated oil and gas company worldwide. The company operates through three segments: Upstream, Downstream, and Chemicals. The Upstream segment engages in the exploration, development, and production of oil and natural gas. It also involves in the transportation, trade, and marketing of natural gas and liquefied natural gas (LNG), as well as in LNG re-gasification and natural gas storage operations. In addition, this segment engages in the shipping and trade of liquefied petroleum gas (LPG); power generation from gas-fired power plants, nuclear, or renewable energies; production, trade, and marketing of coal, as well as in solar power systems and technology operations. As of December 31, 2010, it had combined proved reserves of 10,695 Mboe of oil and gas. The Downstream segment involves in refining, marketing, trading, and shipping crude oil and petroleum products. It also produces a range of specialty products, s uch as lubricants, LPG, jet fuel, special fluids, bitumen, marine fuels, and petrochemical feedstock. This segment holds interests in 24 refineries located in Europe, the United States, the French West Indies, Africa, and China, as well as operates a network of 17,490 service stations. The Chemicals segment produces base chemicals, including petrochemicals and fertilizers, as well as engages in rubber processing, resins, adhesives, and electroplating activities. TOTAL S.A. was founded in 1924 and is based in Paris, France.

Advisors' Opinion:- [By Ben Levisohn]

Shares of French oil giant Total (TOT) have gained 1.9% t $58.27 this morning after Barclays�upgraded the stock to Equal Weight from Underweight.

Associated PressBarclays’�Lydia Rainforth and team explain their reasoning:

Total�� Capital Markets Day presentation did enough to convince us that it can�control capex more than we had previously anticipated. In doing so, it also set out a�more credible path to returning the company to cash flow neutrality post both capex and dividends potentially as soon as 2015. There remain challenges to delivering the 2017 operating cashflow aspiration, as evidenced by an implicit reduction in prior cashflow assumptions over the 2015-2017 period, but the coming 12 months should see Total show both improved production and cashflow with the start up of a number of key projects scheduled. It is this combination of improved operational momentum we forecast for Total together with much better visibility on capex and free cash flow, which drives our upgrade on the stock to Equal Weight…

Total’s strength comes as U.S oil majors have stalled today. Exxon Mobil (XOM) has ticked down 0.1% to $87.69 , Chevron (CVX) has fallen o.4% to $125.07 and�ConocoPhillips (COP) has dropped 0.3% to $70.35.

- [By David Smith]

Bowing out of Egypt

It's also noteworthy that Egypt shares a western border with Libya, which is a significant producer, but where chaos and contretemps also reign. Is it any wonder, then, that Chevron (NYSE: CVX ) announced on Tuesday that it will unload its Egyptian downstream operations, including 66 service stations and a couple of oil depots, to Total (NYSE: TOT ) ? The French company is also buying the retail assets in the land of the Sphinx from Royal Dutch Shell (NYSE: RDS-B ) . Perhaps it knows something of which the rest of us are unaware. - [By Sara Murphy]

HSBC recently conducted an analysis that looked at European oil majors' at-risk carbon reserves. The study found Norway's�Statoil (NYSE: STO ) �to be the worst affected, with approximately 17% of its market capitalization at risk. HSBC also calculated that 6% of�BP's� (NYSE: BP ) reserves are at risk, along with 5% of�Total's (NYSE: TOT ) and 2% of�Shell's� (NYSE: RDS-A ) .�

Top 5 Cheap Stocks For 2014: Wisconsin Energy Corporation (WEC)

Wisconsin Energy Corporation engages in the generation, distribution, and sale of electric energy and steam. The company also involves in the purchase, distribution, and sale of natural gas to retail customers, as well as in the transportation of customer-owned natural gas in Wisconsin. It generates electricity from coal, natural gas, wind, and hydro sources. The company offers its services under ?We Energies? name. It serves approximately 1,120,200 electric customers in Wisconsin and the Upper Peninsula of Michigan; approximately 1,064,500 gas customers in Wisconsin; and approximately 460 steam customers in metropolitan Milwaukee, Wisconsin. In addition, the company invests and develops in real estate properties, including business parks and other commercial real estate projects primarily in southeastern Wisconsin. It provides electric utility service to industries, such as mining, paper, foundry, food products, and machinery production, as well as to retail chains. The c ompany was founded in 1981 and is based in Milwaukee, Wisconsin.

Advisors' Opinion:- [By Larry Smith]

Wisconsin Energy (WEC) - Wisconsin Energy is the largest electric and gas company in Wisconsin with 1.1 million electric customers and 1 million gas customers. Wisconsin Energy also owns a 26% interest in American Transmission Company, a multistate, transmission only utility. WEC has been named the most reliable utility in the Midwest seven out of the last 10 years and has very high customer satisfaction. I owned WEC briefly and would be willing to own it again at a price under $38.00.

Hot Dividend Companies To Watch For 2014: Leggett & Platt Incorporated(LEG)

Leggett & Platt, Incorporated designs and produces various engineered components and products worldwide. Its Residential Furnishings segment offers bedding components, such as innersprings and wire forms; furniture components, including steel mechanisms, springs, seat suspensions, steel tubular seat frames, bed frames, ornamental beds, and power foundations; and structural fabrics, carpet underlay materials, and geo components. This segment serves manufacturers of finished bedding products or upholstered furniture. The company?s Commercial Fixturing & Components segment provides shelving, counters, showcases, and garment racks; standardized shelvings; point-of-purchase displays; and bases, columns, back rests, casters, and frames. This segment offers its products to retail chains and specialty shops; brand name marketers; distributors of consumer products; and office, institutional, and commercial furniture manufacturers. Its Industrial Materials segment provides steel rod s, drawn wires, steel billets, fabricated wire products, welded steel tubing, and fabricated tube components to bedding and furniture, and mechanical spring makers; automotive seating, and lawn and garden equipment manufacturers; and waste recyclers, waste removal businesses, and medical supply businesses. The company?s Specialized Products segment offers manual and power lumbar support and massage systems; seat suspension systems; automotive control cables; low voltage motors; actuation assemblies; formed metal and wire components; quilting machines; machines for shaping wire into springs; industrial sewing/finishing machines; van interiors; and docking stations, as well as specialty trailers for telephone, cable, and utility companies. It serves bedding and automobile seating manufacturers. The company sells its products through its sales representatives and distributors. Leggett & Platt, Incorporated was founded in 1883 and is based in Carthage, Missouri.

Advisors' Opinion:- [By Dividends4Life]

Related Articles:

- Lockheed Martin Corp. (LMT) Dividend Stock Analysis

- 3M Company (MMM) Dividend Stock Analysis

- Leggett & Platt, Inc. (LEG) Dividend Stock Analysis

- McDonald's Corporation (MCD) Dividend Stock Analysis

- More Stock Analysis - [By Oliver Pursche]

I think the first step will be an increase in share-buybacks and an increase in dividends. As such, I am once again overweighting large-cap multinationals, including some great European names. My favorites include Novartis (NVS) , Legget and Platt (LEG) and Visa (V) .� Of course, the potential risk is that the cash horde remains and even grows, likely creating a deeper negative interest rate environment ��something that surely would be damaging to our economy.

- [By Arie Goren]

After running this screen on May 21, 2013, before the markets' open, I discovered the following eight stocks: Sunoco Logistics Partners LP (SXL), Leggett & Platt Inc (LEG), Copa Holdings SA (CPA), RPC Inc. (RES), Tupperware Brands Corp. (TUP), Herbalife Ltd. (HLF), John Wiley & Sons Inc. (JW.A) and C.H. Robinson Worldwide Inc. (CHRW).

Hot Dividend Companies To Watch For 2014: Xcel Energy Inc.(XEL)

Xcel Energy Inc., through its subsidiaries, engages in the generation, purchase, transmission, distribution, and sale of electricity to residential, commercial, and industrial customers, as well as to public authorities in the United States. The company generates electricity using coal, nuclear, natural gas, hydro, wood, diesel, and wind energy. It also engages in the purchase, transportation, distribution, and sale of natural gas to residential, commercial, and industrial customers. The company serves customers in portions of Colorado, Michigan, Minnesota, New Mexico, North Dakota, South Dakota, Texas, and Wisconsin. As of December 31, 2010, it provided electricity services to 3,391,611 customers; and natural gas services to 1,893,250 customers. Xcel Energy, through its joint venture interests in WYCO Development LLC, develops and leases natural gas pipeline, storage, and compression facilities. The company was founded in 1909 and is based in Minneapolis, Minnesota.

Advisors' Opinion:- [By Sean Williams]

Another risk factor that can often be overlooked is that electricity price increases aren't a guarantee. In fact, power price increase rulings are often determined by state regulatory energy commissions which have a duty to look out not for these companies, but also for the best interests of consumers. Last summer, for instance, Xcel Energy (NYSE: XEL ) was denied a $100 million rate increase (about $2 each month per customer) by the Colorado Public Utilities Commission after failing to sufficiently demonstrate how not raising these rates would adversely impact the company.�

Monday, October 14, 2013

5 Best Dividend Stocks To Invest In 2014

LONDON -- I'm looking at some of your favorite FTSE 100 companies and examining how each will deliver their dividends.

Today, I'm putting Anglo-Dutch consumer goods giant�Unilever� (LSE: ULVR ) (NYSE: UL ) under the microscope.

Dividend policy

Soon after Paul Polman took over as chief executive in January 2009, Unilever announced a new dividend policy to run from 2010 onward:�"Unilever's policy is to seek to pay an attractive, sustainable and growing dividend to shareholders."

The company said it would move from paying an interim and final dividend each year to paying four quarterly dividends, announced with the quarterly results. It added that the change would�"better align the payments with the cash flow generation of the business."

Dividend delivery

The table below shows the extent to which Unilever has grown its dividend since the move to quarterly payouts. It should be noted that the company's reporting currency is the euro. Thus, the euro dividend is the gauge for measuring performance against policy, while the sterling dividend is at the mercy -- for better or worse -- of prevailing exchange rates.

5 Best Dividend Stocks To Invest In 2014: Capital Bank Corporation(CBKN)

Capital Bank Corporation operates as the holding company for Capital Bank that provides general commercial banking products and services in North Carolina. Its deposit products include checking, savings, negotiable order of withdrawal, money market, and individual retirement accounts, as well as certificates of deposit. The company?s loan products portfolio comprises loans for real estate, construction, businesses, agriculture, personal use, home improvement, and automobiles, as well as equity lines of credit, mortgage loans, credit loans, consumer loans, and credit cards. It also offers safe deposit boxes, bank money orders, Internet banking services, traveler?s checks, and notary services, as well as electronic funds transfer services, including wire transfers and remote deposit capture. In addition, the company provides automated teller machine access to its customers; and a line of uninsured investment products and services. It operates 32 branch offices in North Carol ina, including 5 in Raleigh, 4 in Asheville, 4 in Fayetteville, 3 in Burlington, 3 in Sanford, 2 in Cary, and 1 each in Clayton, Graham, Hickory, Holly Springs, Mebane, Morrisville, Oxford, Pittsboro, Siler City, Wake Forest, and Zebulon. The company was founded in 1997 and is headquartered in Raleigh, North Carolina. Capital Bank Corporation is a subsidiary of North American Financial Holdings, Inc.

5 Best Dividend Stocks To Invest In 2014: Cedar Shopping Centers Inc (CDR)

Cedar Shopping Centers, Inc., real estate investment trust, engages in the ownership, operation, development and redevelopment of supermarket-anchored community shopping centers and drug store-anchored convenience centers in the United States. As of December 31, 2007, it owned 118 properties, aggregating approximately 12.0 million square feet of gross leasable area primarily in Pennsylvania, Massachusetts, Virginia, Ohio, Connecticut, New Jersey, Maryland, Michigan, and New York. Cedar Shopping has elected to be treated as a REIT for federal income tax purposes and would not be subject to federal income tax, if it distributes at least 90% of its REIT taxable income to its stockholders. The company was founded in 1984 and is based in Port Washington, New York.

Advisors' Opinion:- [By Bill Smith]

Valuation

Lastly, because of the negative perception the entire industry has received, prices in this sector have been absolutely pummeled. ESI now trades at the lower end of all of its historical valuation bands: P/E, P/B, and P/S.

Bullish Points

Guru ownership and avg price: ESI owned by Hussman ($76.15), Weitz ($75.32), and Greenblatt ($73.29)Over 35% of shares are short, potential short squeezeStock buyback plan: ESI reduced outstanding shares by 19% yoy at the end of the 4th quarter. They repurchased 370K shares in 3Q11.The business model is scalable; the incremental cost to educate each additional student is low, leading to high marginsESI acquired Daniel Webster College, giving them a regional accreditation which they can use to broaden their reach in online classes

Bearish Points

High costs of education, in general, rightly or wrongly attract government intervention and could squeeze margins over time. Total student debt surpassed credit card balances, and sits at $1 Trillion as of the end of 2011.Subject to compliance with Dept of Education's 90/10 rules, which states a college can't collect more than 90% of revenue from students participating in federal loan programs.Cohort Default Rate (CDR): for-profit colleges must monitor the federal loan default rates of students who graduate or leave the school. If a school's CDR exceeds 25% for 3 consecutive years, or 40% in any one year, its students won't be eligible for federal financial aid.ESI competes on quality of product which is measured by graduation rates and ability to secure employment. For 2010, 70% of ESI graduates got employment in positions using skills taught in their program of study within 1 year. As of Oct 2011, this rate was 600 bp higher. The average annual salary reported by employed 2011 grads was $32K, compared to $32.4K for 2010 grads.With an improving economy, there's a potential ESI would see declining new student enrollmentsOver 35% of shares are short

Summary

Hot Energy Stocks To Watch For 2014: Smith & Nephew SNATS Inc.(SNN)

Smith & Nephew plc develops, manufactures, markets, and sells medical devices in the orthopaedics, endoscopy, and advanced wound management sectors worldwide. The company operates in three segments: Orthopaedics, Endoscopy, and Advanced Wound Management. The Orthopaedics segment offers reconstruction implants, including hip, knee, and shoulder joints, as well as ancillary products, such as bone cement and mixing systems used in cemented reconstruction joint surgery. This segment also provides trauma fixation products consisting of internal and external devices, and other products, including shoulder fixation and orthobiological materials used in the stabilization of fractures and deformity correction procedures; and clinical therapies products comprising bone growth stimulation, joint fluid therapies, and outpatient spine products. The Endoscopy segment develops and commercializes minimally invasive surgery techniques, educational programs, and value-added services for sur geons to treat and repair soft tissue and articulating joints. It offers specialized devices and fixation systems to repair damaged tissues; fluid management equipment for surgical access; digital cameras, digital image capture, scopes, light sources, and monitors to assist with visualisation; radiofrequency wands, electromechanical and mechanical blades, and hand instruments for resecting damaged tissues. The Advanced Wound Management segment provides initial wound bed preparation and full wound closure products. This segment?s products are targeted at chronic wounds associated with the older population, such as pressure sores and venous leg ulcers; and products for the treatment of wounds, including burns and invasive surgery. The company serves medical and surgical service providers. Smith & Nephew plc was founded in 1856 and is headquartered in London, the United Kingdom.

Advisors' Opinion:- [By Charles Carlson, CEO and Portfolio Manager, Horizon Investment Services]

For investors looking for growth but also income, I especially like three health-care related stocks��resenius Medical (FMS), Novo Nordisk (NVO), and Smith & Nephew (SNN).

- [By Sean Williams]

Smith & Nephew (NYSE: SNN ) : 2.6% projected forward yield

Smith & Nephew is a U.K.-based medical-device maker that targets orthopedic reconstructive implants such as hip and knee replacements, and advanced wound management care products such as Durafiber and Acticoat for infection prevention. In the most recent quarter, Smith & Nephew delivered double-digit emerging-market growth (something my Foolish colleague Dan Carroll recently pointed out), while weak European growth caused sales in that region to be flat. Its sports medicine segment also delivered solid growth of 6%. - [By Dan Carroll]

British device maker Smith & Nephew (NYSE: SNN ) is the latest company�to join the emerging markets push. The company announced it agreed to buy Indian trauma device maker Adler Mediequip, which -- along with the buyout of a Brazilian�distribution partner -- totaled around $70 million. What does this mean for your investment and the medical device industry's emerging markets momentum?

- [By Kevin Godbold]

So this series aims to identify appealing FTSE 100 investment opportunities and today I'm looking at�Smith & Nephew� (LSE: SN ) (NYSE: SNN ) , the medical devices company.

5 Best Dividend Stocks To Invest In 2014: Microchip Technology Incorporated(MCHP)

Microchip Technology Incorporated, together with its subsidiaries, develops, manufactures, and sells semiconductor products for various embedded control applications. It offers a family of microcontroller products that include 8-bit, 16-bit, and 32-bit PIC microcontrollers; and 16-bit dsPIC digital signal controllers, which feature on-board flash memory technology. The company also provides a set of application development tools that enable system designers to program a PIC microcontroller and dsPIC DSC for specific applications. In addition, it offers analog and interface products, which consist of various families with approximately 600 power management, linear, mixed-signal, thermal management, safety and security, and interface products. Further, the company provides memory products comprising serial electrically erasable programmable read-only memory. Its products are used in various applications in automotive, communications, computing, consumer, and industrial contr ol markets. Microchip Technology Incorporated markets its products primarily through a network of direct sales personnel and distributors in the Americas, Europe, and Asia. The company was founded in 1989 and is based in Chandler, Arizona.

Advisors' Opinion:- [By Jon C. Ogg]

Microchip Technology Inc. (NASDAQ: MCHP) was raised to Buy from Neutral with a $46 price target at Goldman Sachs.

Network Appliances Inc. (NASDAQ: NTAP) was downgraded to Equal Weight from Overweight with a new $46 price target by Barclays.

- [By Beth Piskora]

They are listed below:

Altera (ALTR)��ielding 1.7%

Apple (AAPL)��ielding 2.5%

Applied Materials (AMAT)��ielding 2.6%

Cisco (CSCO)��ielding 2.9%

EMC Corp. (EMC)��ielding 1.5%

International Business Machines (IBM)��ielding 2.0%

KLA-Tencor (KLAC)��ielding 3.2%

Microchip Technology (MCHP)��ielding 3.6%

Oracle (ORCL)��ielding 1.5%

Qualcomm (QCOM)��ielding 2.1%

Texas Instruments (TXN)��ielding 2.9%

Xilinx (XLNX)��ielding 2.3%

Subscribe to S&P's The Outlook here��/P>

- [By CRWE]

Microchip Technology Incorporated (NASDAQ:MCHP), a leading provider of microcontroller, analog and Flash-IP solutions, reported that its Board of Directors has declared a quarterly cash dividend on its common stock of 35.1 cents per share.

5 Best Dividend Stocks To Invest In 2014: Dreyfus Municipal Income Inc.(DMF)

Dreyfus Municipal Income, Inc. is a close ended mutual fund launched and managed by The Dreyfus Corporation. It invests in the fixed income markets. It primarily invests in municipal bonds. Dreyfus Municipal Income, Inc. is domiciled in United States.

Sunday, October 13, 2013

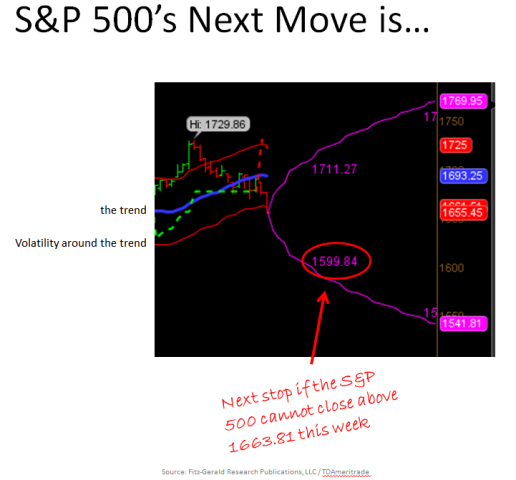

The S&P 500's Point of "No Return"

If you're like most folks, there's a nagging fear at the edge of your brain that's trying desperately to make sense of what's happening each day the market drops further.

It's tough to control under normal circumstances, but even tougher to dismiss against the backdrop of Washington's infantile behavior.

I know... I feel it too - which is why, at moments like the present, I turn to my charts.

There's no guesswork and no ambiguity with charts. Just good old-fashioned technical analysis that is void of all emotion and free from the second guess that all too often interferes with our decisions.

That allows me to calmly, methodically answer a number of questions, including the one I'm getting most right now.

What's the point of "no return"?

The chart of the S&P 500 I constructed Tuesday gives us some clues.

Take a look...

Now let me tell you what you're looking at...

The red lines represent expected price movement and volatility around the trend. That's the blue line that runs according to a proprietary non-linear set of calculations I created.

You can see that Tuesday's close took the S&P 500 down to 1655.03, which is just below the lower red line, which rests at 1663.81. At the same time, the blue line has begun to roll over. It's visually almost unperceivable so you have to look hard.

Best Insurance Stocks To Buy For 2014

There are two key takeaways:

The S&P 500 has already bounced off of support; andIf the SPX does not close above 1663.81 this week, the next stop is 1599.84 by Oct. 18, 2013.

To that end, there is a tremendous battle being fought between the bulls and the bears as I write this. What's sad is that Washington is providing both with plenty of ammo.

So now what?

That's actually the interesting part...

Three Actions You Can Take NowMany investors think that the world's about to end, especially when they see a chart like this.

Nothing's farther from the truth - the markets move up and down all the time. The key is learning how to move with them rather than trying to second guess them. That way you are constantly on the offensive rather than being forced into a purely reactionary posture.

To that end, I think investors should be doing three things right now:

Taking profits. Any move to the downside spells an opportunity to do so... if you've been handling the upside properly. Most investors don't, which is why they fear down days. The easiest way to do that is via trailing stops, which are typically percentage or dollar based. More sophisticated investors can use purchase put options to accomplish the same thing.Hunting for beaten down companies. The uninformed run for cover. On the other hand, guys like Rogers, Mobius, and Soros are the legends they are because they often wade in when others can't see the upside they do. You'd be wise to emulate them.

This bothers some people. But wouldn't you rather buy something when it's put on sale (like it is when the markets are in a foul mood) than when it's too expensive (like it's been)? Energy is my favorite sector right now because it's largely immune from government swings and has built-in long-term demand that's growing. Plus, many companies kick off hefty dividends.

Hedging their bets. Most investors don't understand that specialized inverse funds can be used to take the sting out of falling stock prices. That's because holding 3% to 5% in non-correlated assets can significantly dampen overall portfolio volatility by zigging when everything else zags. In that sense, and if for nothing else, they're great for helping you keep perspective when the stuff hits the fan.

And if the markets do close above 1663.81?

Chances are you'll be glad you stayed on board with upside exposure. I can easily envision the Fed kicking in more money to compensate for political incompetence, especially if Yellen is actually confirmed as the incoming Fed Chief.

In that case, the initial target is 1711.27...

Friday, October 11, 2013

Don't Let Shutdown, Default Anxiety Influence Investments